The State of Consumer AI. Part 2: Engagement and Retention

Usage makes headlines. Habits build franchises.

Consumer markets follow a power law. Every major platform cycle produces one dominant winner that captures disproportionate value. Google took 90%+ of search. Facebook took social. Apple took mobile profits. The pattern is so consistent it’s almost a law of nature: consumer markets don’t split evenly. They concentrate.

As we showed in Part 1, consumer AI is following the same script. ChatGPT holds ~70% market share. Gemini sits at ~20%. Everyone else is fighting over scraps.

But market share alone doesn’t tell you whether a winner is durable. The history of consumer technology is littered with products that spiked in usage and then faded. Remember Google Wave? Clubhouse? BeReal? Clubhouse hit 10M downloads in its first month. BeReal was the #1 app in the App Store. Neither built a habit. Not all usage is created equal. A user who opens an app once a month out of curiosity is fundamentally different from one who opens it every day out of habit. The real question isn’t who has the most users. It’s who has the most habitual users. And that’s where engagement and retention come in.

Part 2 goes a layer deeper. Usage tells you who showed up. Engagement and retention tell you who stayed, and whether they’re forming a habit or just browsing. How often are people actually using these products? Are they sticky enough to survive a better or cheaper competitor? These are the questions that separate a market leader from a durable franchise.

Bottom line up front: ChatGPT is not just the largest AI app. It is also the stickiest. And it is getting stickier. Looking at three years of engagement and retention data, three findings stood out:

ChatGPT’s engagement lead is wider than its market-share lead among AI peers.

Zooming out, ChatGPT has better engagement than most enterprise apps (Slack, Gmail, Outlook) and matches the engagement levels of consumer staples like Facebook, Spotify, and X.

On retention, the same pattern holds. ChatGPT has significantly better retention than AI peers and top enterprise apps, and is steadily converging with the best consumer platforms.

1. ChatGPT’s engagement lead is wider than its market-share lead

In Part 1, I showed that ChatGPT commands ~70% of AI WAU and Gemini is second at ~20%. The engagement data tells an even more concentrated story.

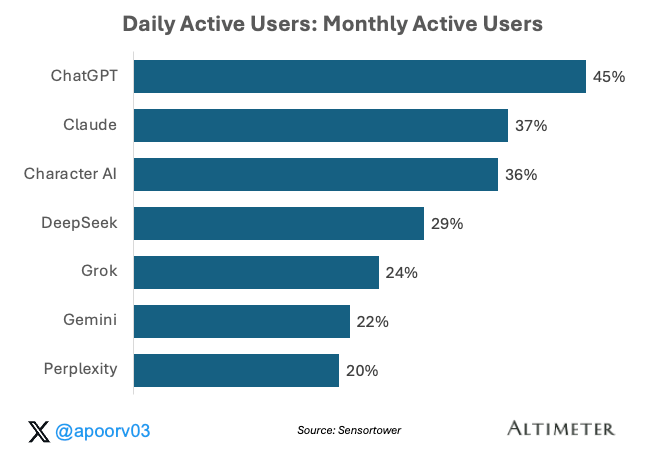

On daily engagement (DAU:MAU), ChatGPT is at 45%. Gemini is at 22%. That is more than a 2x gap. Gemini’s reported MAU is impressive (they reported 750M on the last earnings call), but DAU:MAU tells you more about depth of usage. MAU tells you how many people tried the product in a month. DAU:MAU tells you how many of them are actually using it as part of their day. On that metric, ChatGPT is in a different league.

2. ChatGPT has entered consumer-grade engagement territory

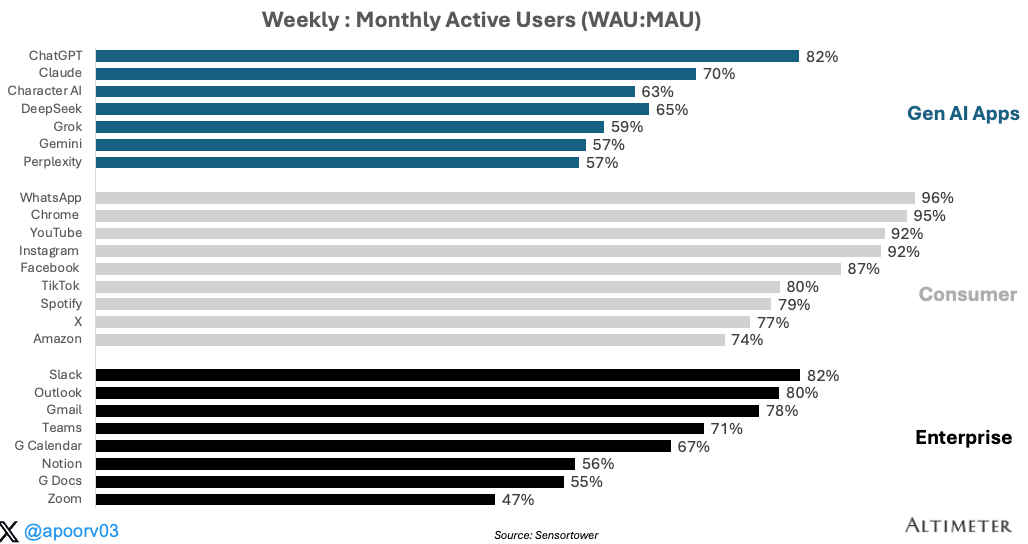

Let’s zoom out beyond AI and compare the new AI app category with established consumer and enterprise applications. And let’s use WAU:MAU because it captures the rhythm of knowledge-work better: people use enterprise apps a few days a week, not every single day.

To put these numbers in context: WhatsApp is at 96%. Instagram is at 92%. Gmail is at 78%. Spotify is at 79%. ChatGPT’s engagement is better than Gmail / Spotify and nearing Instagram, which is remarkable for a product that is three years old and doesn’t have a social graph, a notification-driven feed, or an inbox that fills up on its own. And it’s improving:

Three years ago, ChatGPT’s WAU:MAU was around 50%. I argued at the time that apps need 80%+ WAU:MAU to reach a billion users. Historical data across decades of consumer and enterprise apps showed that engagement levels are largely set by a product’s category and core value proposition.

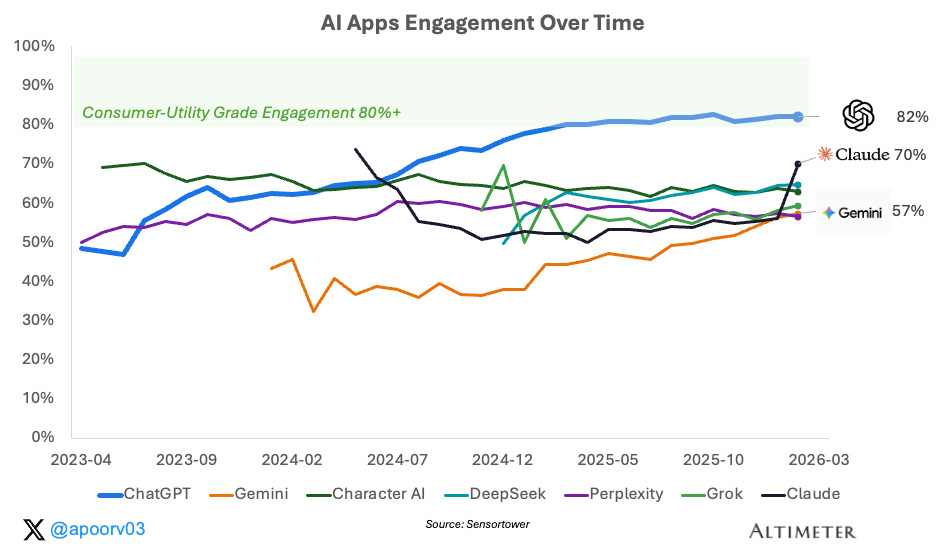

ChatGPT broke that pattern. Its WAU:MAU has gone from ~50% in mid-2023 to 82% today. That is a 30+ percentage point improvement. No other AI app comes close except for Claude which seems to be catching up (a quiet standout and a huge leap over the last month).

The implication: ChatGPT is no longer engaging like an AI curiosity. It is engaging like a tool people rely on every week. The engagement profile matches my Part 1 thesis: ChatGPT is behaving like a utility, not a social app. People don’t scroll it for dopamine. They open it because they need it.

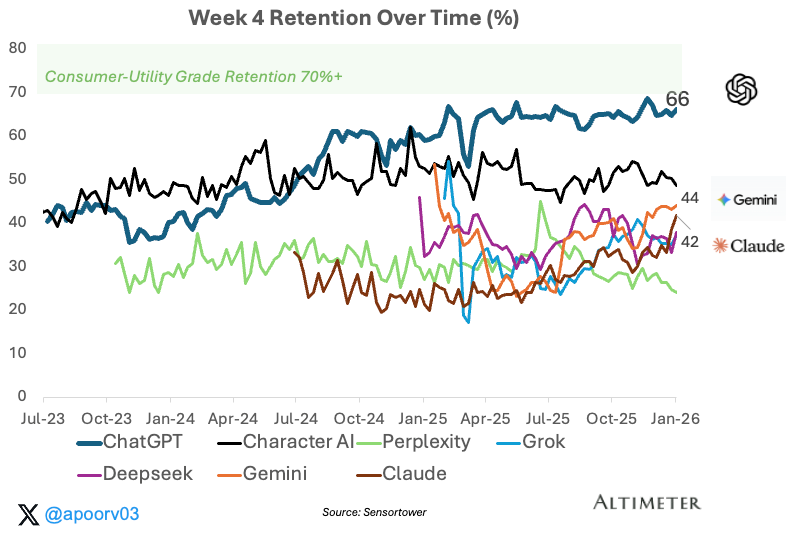

3. The smile curve: ChatGPT is getting stickier over time

Engagement tells you how often people come back in a given window. Retention tells you whether they stick around at all. And the rarest signal in consumer products is whether a product can win back the users who left.

There are three shapes a retention curve can take after the initial drop-off: declining, flattening, or smiling. I covered these in my original analysis two years ago. Most apps flatten or decline. A smile curve, where retention dips and then recovers, is the rarest. That likely reflects product improvements pulling users back in.

In our dataset, very few products show a true smile curve in retention, with rare examples including Gmail, ChatGPT, and Chrome. That’s it. WhatsApp, Instagram, TikTok, Spotify, Slack, Outlook, YouTube: all flat or declining curves. They hold users well, but they don’t win them back over time. ChatGPT does. And it’s doing it at 900M WAUs, which means OpenAI’s pace of product iteration (voice, vision, canvas, search, memory) is not just attracting new users but reactivating lapsed ones.

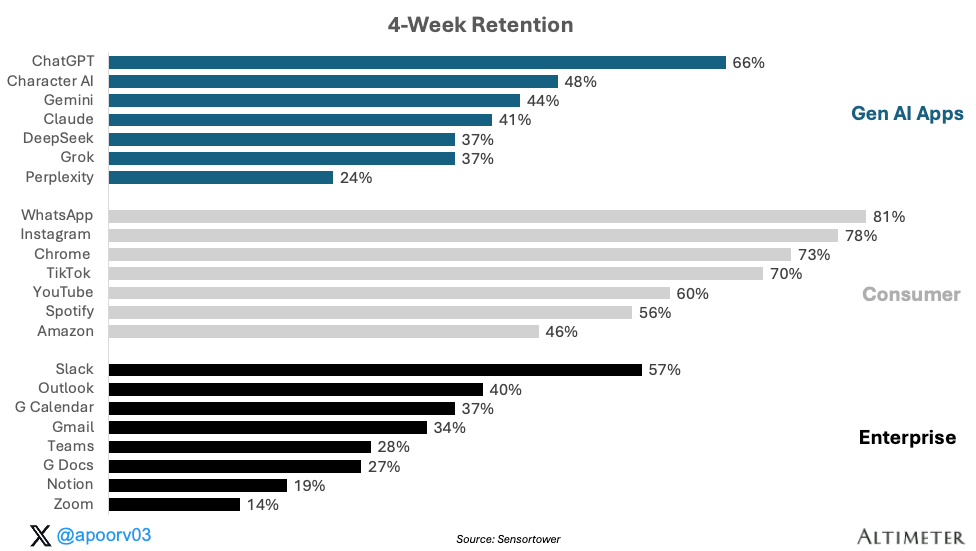

The floor is already high

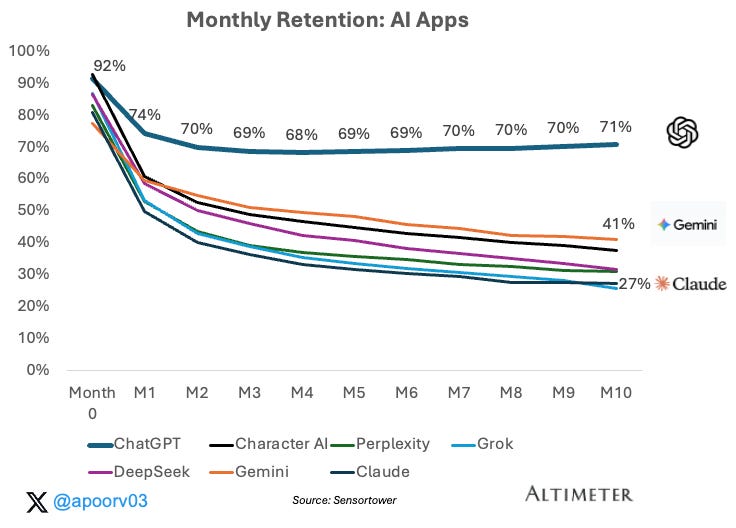

The smile curve is even more notable given where retention starts. At Week 4, ChatGPT retains ~66% of its users. Two out of three people who download it are still active four weeks later.

Among AI apps, the gap is material: Character AI is at 48%, Gemini 44%, Claude 41%, Perplexity 24%. At 66%, ChatGPT is building an installed base. At 24%, Perplexity is still struggling to build an installed base on mobile.

Against established apps, ChatGPT’s Week 4 retention beats every enterprise app in our dataset, including Slack. It trails the top consumer utilities (WhatsApp, Instagram, Chrome) but sits in the same range as TikTok. Two years ago, I plotted adoption against retention and found the same clustering: consumer apps top-right, enterprise apps in the middle, AI apps bottom-left. ChatGPT has since migrated out of the AI cluster and into enterprise territory, approaching consumer.

Retention that improves at scale

Three years ago, ChatGPT’s Week 4 retention was closer to 40%. It has climbed to 66% today, a roughly 25 percentage point gain. Most apps see retention set early and stay flat or decline as the user base matures and more casual users come in. ChatGPT has done the opposite: as its user base has grown 10x, retention has gotten better. The most likely explanation is product improvement. Each major release has given users a new reason to come back.

That trajectory is what makes the smile curve credible. ChatGPT isn’t recovering from a weak starting point. It’s recovering from an already-strong floor, and doing so while adding hundreds of millions of users. That combination is genuinely rare.

Conclusion

ChatGPT is no longer just the biggest AI app. It is becoming one of the stickiest products on the internet. High weekly engagement, strong early retention, and improving stickiness even at massive scale. That is not novelty. That is habit formation.

And in consumer technology, habit is what separates reach from revenue. A product with 900 million weekly users and improving retention is not just winning attention. It is building a franchise.

For competitors, the window to displace ChatGPT is narrowing. Not because the product is unbeatable, but because the habit is compounding. Every week that engagement and retention improve at this scale, switching costs go up and the gravitational pull gets stronger.

Part 3 next week will look at time spent and what that tells us about monetization.

Sources used in this post include Sensortower.

The information presented in this newsletter is the opinion of the author and does not necessarily reflect the view of any other person or entity, including Altimeter Capital Management, LP (”Altimeter”). The information provided is believed to be from reliable sources but no liability is accepted for any inaccuracies. This is for information purposes and should not be construed as an investment recommendation. Past performance is no guarantee of future performance. Altimeter is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. Altimeter and its clients trade in public securities and have made and/or may make investments in or investment decisions relating to the companies referenced herein. The views expressed herein are those of the author and not of Altimeter or its clients, which reserve the right to make investment decisions or engage in trading activity that would be (or could be construed as) consistent and/or inconsistent with the views expressed herein.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.

Why does this sound like an ad for Chat GPT? The reality is that switching costs between LLMs is zero. There are no network effects and you can even take your data with you to a new LLM. The fact is that LLMs are commoditizing and for the vast majority of tasks, you’ll soon be able to run a capable open source LLM on your laptop (e.g. Gemma version 5). In fact, you already can with a MacBook with 64 gb of memory. The future looks pretty bleak for ChatGPT from this perspective!

Past performance does not indicate future performance. All three parts of this series break this paradigm.

Exceptional content, very deep analysis. Thank you!