The State of Consumer AI. Part 1: Usage

Two years ago, I argued that consumer AI was heading toward a familiar endgame: distribution would trump raw model quality, and hence the incumbents Google and Meta were best positioned to win. Back then, ChatGPT had ~100M weekly active users.

That debate has played out. I was wrong.

Today, AI apps have crossed 1 billion weekly active users and ChatGPT alone accounts for 900M of that. It built that user base from scratch, without an existing distribution platform. Below I analyze usage data across apps to make the case that ChatGPT is the only AI app with both the installed base and new user momentum to become a core utility, like WhatsApp and Chrome are today. Every other challenger wave has faded. ChatGPT keeps compounding.

This is Part 1 of a multi-part series focused on usage. Engagement, retention, and time spent are next. I analyze usage across four dimensions:

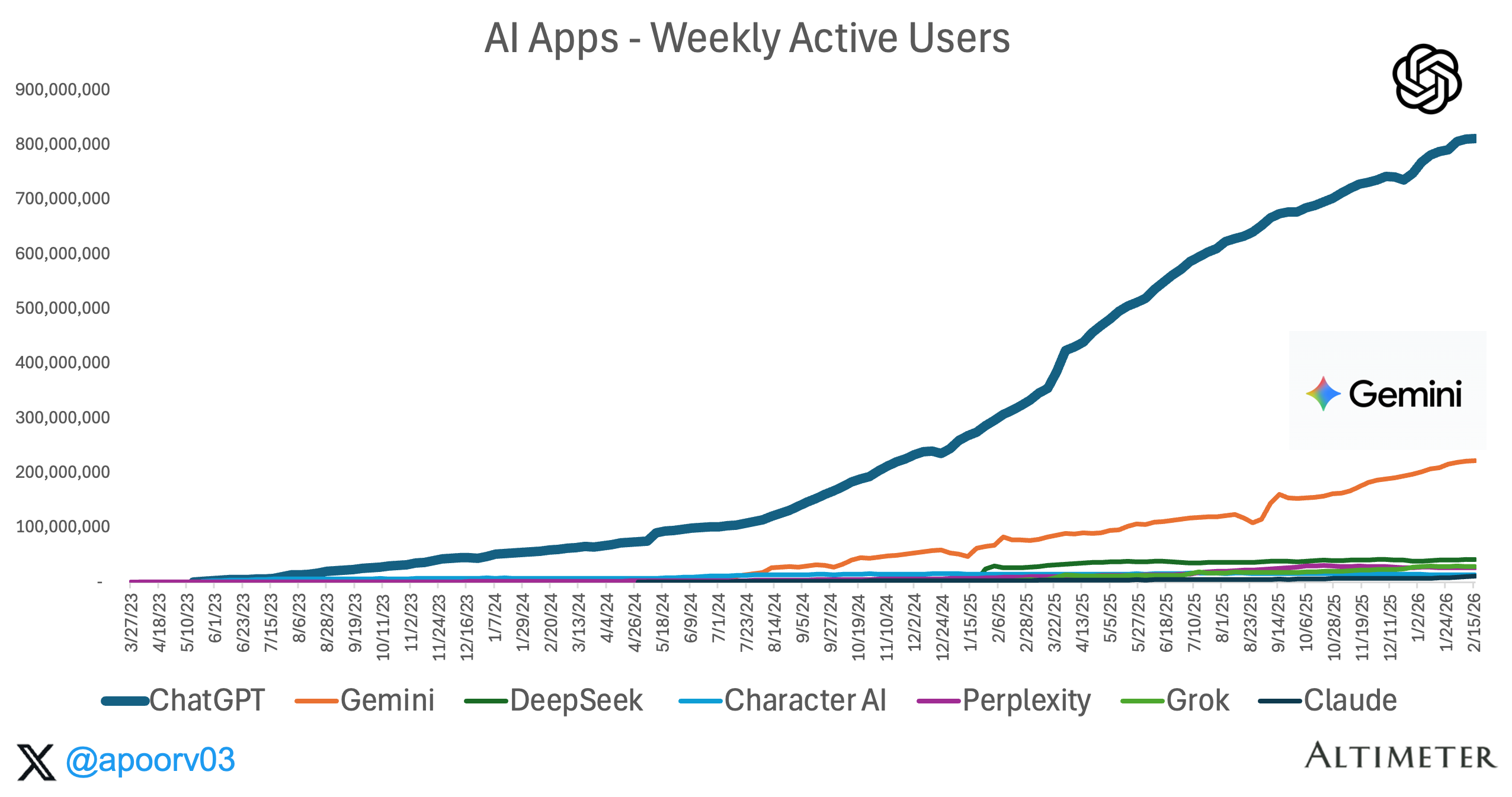

ChatGPT pulls away in a two-horse AI race

ChatGPT vs. the Consumer giants: closer than you think

Four seasons of the year: OpenAI, Google, XAI, China

Among AI apps, only ChatGPT looks like a plausible new utility

1. ChatGPT pulls away in a two-horse AI race

Source: Sensortower

Methodology note: Source is Sensortower, so this analysis is mobile-only and likely understates web-heavy AI usage. I use weekly active users because it is a useful midpoint between DAU and MAU and a reasonable way to compare emerging AI products against established consumer apps.

Total AI app WAUs have gone from ~100M in January 2024 to over 1.2 billion in February 2026. That is a roughly 20x increase in two years. No app category in history has scaled this fast.

ChatGPT at 900 million WAUs is larger than Spotify at ~600 million, in the same neighborhood as TikTok (~1.5B) and Instagram (~1.3B), and approaching WhatsApp and Chrome (~2.5B each) which I consider essential utilities. When I wrote the original post, ChatGPT was a rounding error next to consumer giants. Now it’s in the same league. Most people, myself included, thought this would take much longer.

Source: Sensortower

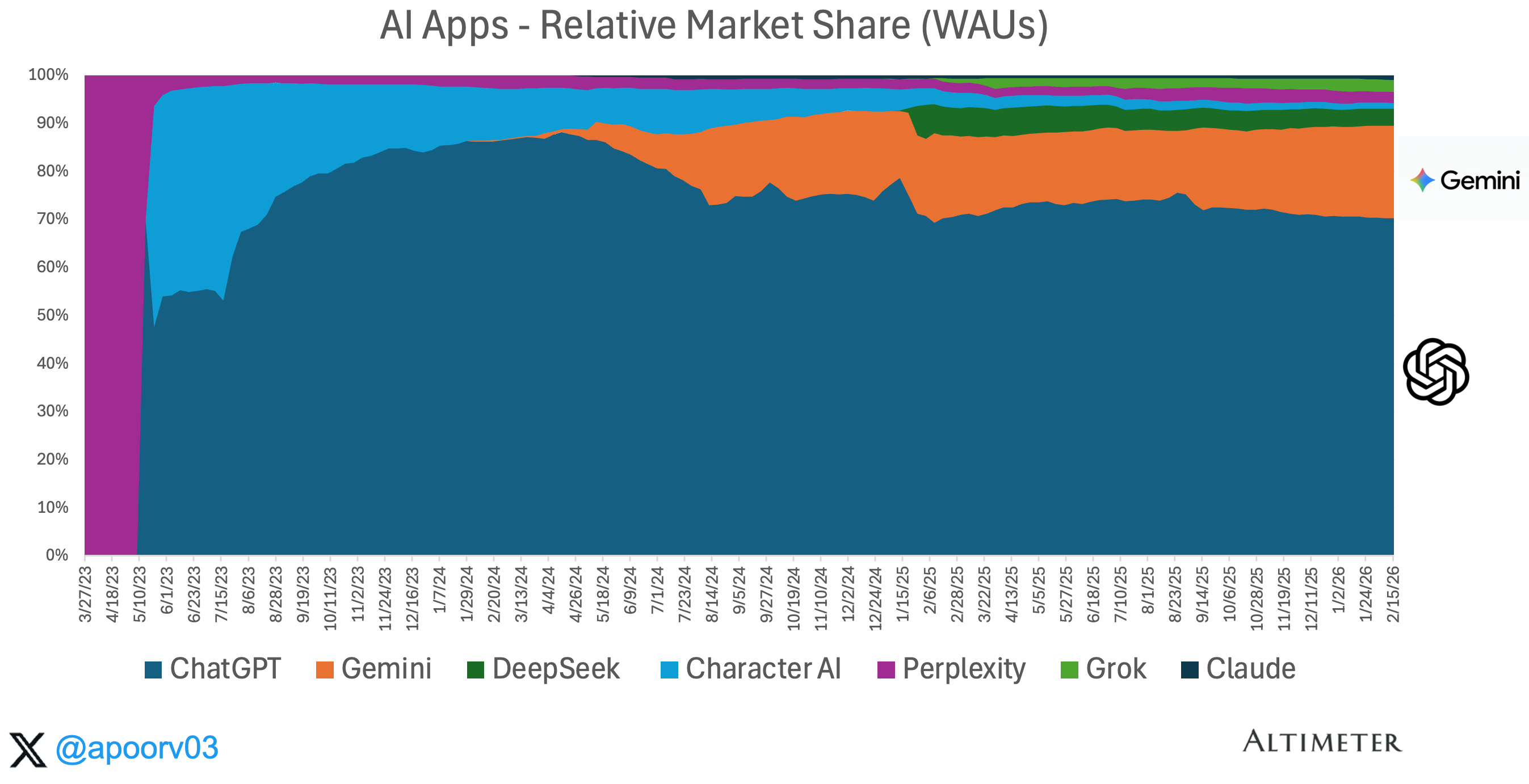

ChatGPT commands approximately 70% of total AI WAU. It has held that share consistently for the past year. Gemini accounts for roughly 15-20%. Everyone else (DeepSeek, Grok, Perplexity, Claude, Character AI) combines for ~10%.

The AI category grew 20x, but almost all of that growth accrued to two apps. ChatGPT built its user base from scratch, without an existing distribution platform. Gemini is riding Google’s 4-billion user distribution.

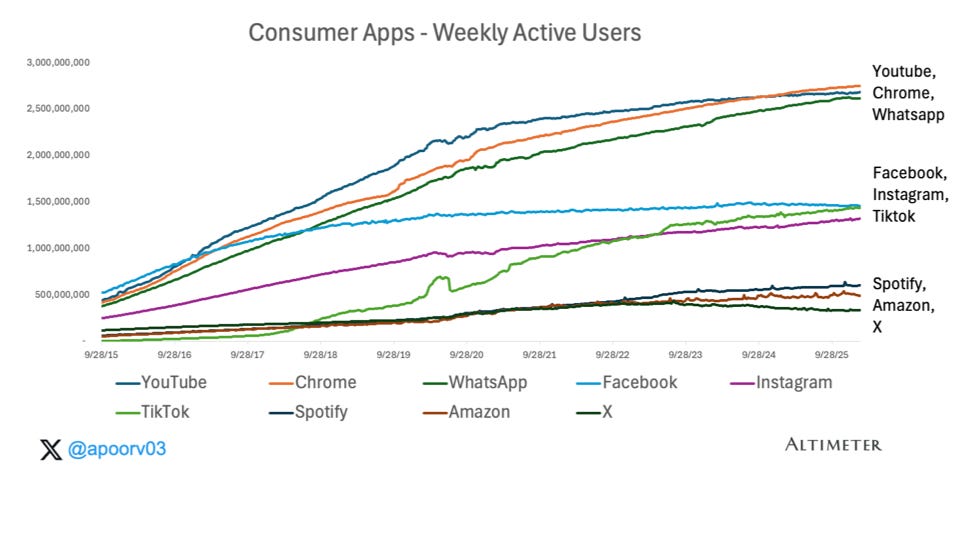

2. ChatGPT vs. the Consumer giants: closer than you think

To understand where AI apps fit, it helps to look at how consumer apps have stratified over the past decade.

Source: Sensortower

Consumer app usage has settled into three tiers:

Core Utility (~2-3B WAU): YouTube, Chrome, WhatsApp. These are infrastructure. Apps so embedded in daily life that they function more like operating system features than standalone products. Growth is slow and steady, driven by smartphone penetration rather than viral loops.

Social platforms (~1-1.5B WAU): Facebook, Instagram, TikTok. Habitual-use apps driven by content graphs and social reinforcement. They took years to climb into this tier and growth has largely plateaued.

Niche apps (~300-600M WAU): Spotify, Amazon, X. Category leaders with enormous user bases that serve more specific needs. Usage is frequent but not universal.

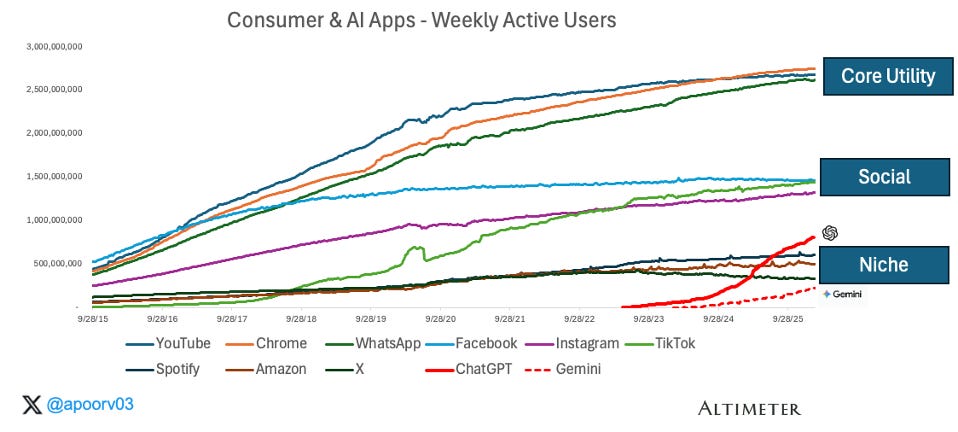

AI is no longer just a category to benchmark against itself. It now belongs on the same chart as the biggest consumer products ever built:

ChatGPT, at 800-900M WAU, cleared the niche tier and is now moving toward the social tier. It did so in roughly three years, a timeline that took Instagram five and TikTok four. Gemini, at roughly 200M WAU, is entering the “Niche” tier from below.

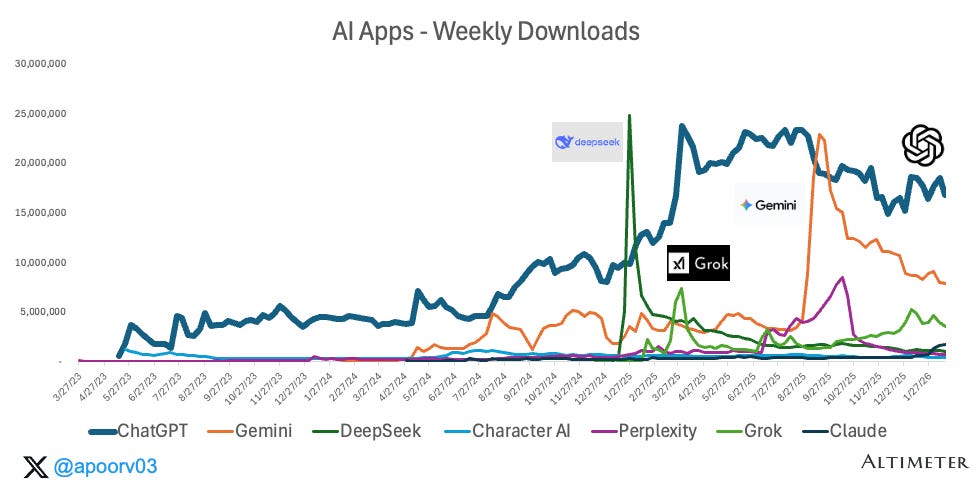

3. Four seasons of the year: OpenAI, Google, XAI, China

The WAU chart tells a story of concentration. The download chart tells a story of chaos.

Source: Sensortower

Over the past year, each season brought a different challenger into the spotlight, each riding a wave of hype, product launches, or distribution muscle. Think of it as four seasons of AI downloads:

Winter 2025: China. DeepSeek exploded past 25 million weekly downloads in January 2025, briefly rivaling ChatGPT’s own numbers. The open-source model’s performance caught the industry off guard and triggered a wave of “is OpenAI in trouble?” commentary. Within weeks, downloads fell back to a fraction of their peak.

Spring 2025: XAI. Grok rode a surge through Q1 and into Q2, fueled by Elon Musk’s distribution via X and a string of model updates. Downloads spiked, press coverage followed. But sustained usage never materialized at the same scale.

Summer 2025: Google. Gemini’s biggest moment. Weekly downloads surged above 20 million, driven largely by the nano banana model — Google’s viral image generation release around Google I/O. The spike was almost entirely image-gen related, which also explains the subsequent drop: it was a model moment, not a sustained behavior shift. Google’s distribution engine likely amplified the reach, but the catalyst was having a genuinely good image model that created viral sharing.

Every season: OpenAI. Through all of it, ChatGPT kept compounding. While each challenger grabbed headlines for a quarter, ChatGPT’s download numbers remained consistently at or near the top, week after week, with none of the volatility. The steady line on the chart is the one that matters.

Honorable mention: Anthropic. As of this writing, Claude hit #1 free app in the App Store. Whether this becomes another seasonal spike or something more durable is worth watching. But the pattern so far has been clear: attention is easier to capture, daily habits are hard to build.

The pattern is clear. Each quarter produces a new “threat to ChatGPT” narrative. Each one fades. Downloads spike on hype. Usage accrues to the apps that earn daily habits.

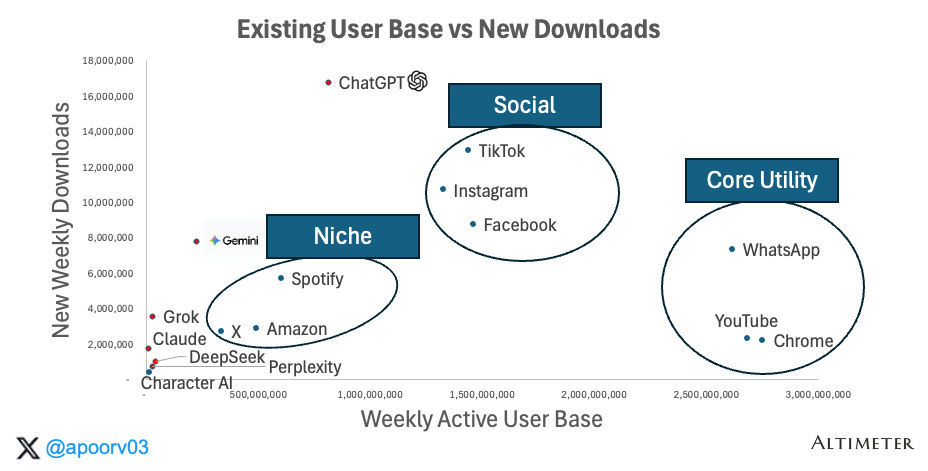

4. Among AI apps, only ChatGPT looks like a plausible new utility

I think about consumer apps through the lens of stock and flow. Stock is your current user base. Flow is new downloads. Plot both and you get a clear picture of momentum:

Source: Sensortower

This scatter plot captures the end result. ChatGPT occupies a position that, among consumer apps, only the core utility apps (WhatsApp, YouTube, and Chrome) and the dominant social apps (TikTok, Instagram, and Facebook) share. A massive existing user base and high new downloads. Gemini is pulling meaningful downloads but hasn’t converted them into a comparable installed base yet. The rest of the AI field is clustered in the bottom-left: small base, modest downloads. Unless something dramatic changes, ChatGPT is the only AI app on a path to a “Core Utility”.

Conclusion

AI apps have crossed a billion weekly active users. ChatGPT owns 70% of that and is the only AI app operating at true consumer internet scale, reaching 800-900M WAUs in roughly three years without an existing distribution platform.

Google is a real but distant second. Gemini at 200-250M WAUs is the only other AI app that has converted downloads into durable usage, largely by leveraging Android, Search, and 4 billion existing users. No one else is close.

But not all usage is equal. In Part 2, we’ll look at engagement, where ChatGPT’s lead is even more pronounced across DAU:MAU ratios, retention, and time spent.

In consumer markets, once one product owns both the installed base and the flow of new users, the default outcome is further consolidation. ChatGPT has both. The question now is whether that usage is deepening into genuine habit or still behaving like a utility people visit briefly and leave. That’s the real battleground from here.

* * *

Sources used in this post include Sensortower.

The information presented in this newsletter is the opinion of the author and does not necessarily reflect the view of any other person or entity, including Altimeter Capital Management, LP (”Altimeter”). The information provided is believed to be from reliable sources but no liability is accepted for any inaccuracies. This is for information purposes and should not be construed as an investment recommendation. Past performance is no guarantee of future performance. Altimeter is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. Altimeter and its clients trade in public securities and have made and/or may make investments in or investment decisions relating to the companies referenced herein. The views expressed herein are those of the author and not of Altimeter or its clients, which reserve the right to make investment decisions or engage in trading activity that would be (or could be construed as) consistent and/or inconsistent with the views expressed herein.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.

Great post ! Back to your original argument, the luck of ChatGPT is that Google can't go full steam on embedding gemini everywhere due to the change of business model. Still, AI overview and AI modes are expanding fast and, I guess, hard to measure so reality in terms of time spent might be more complex (but reading now your next piece :))

Wasn't aware that claude, which I felt is much better than gptfor personal use, is this behind Openai.