The State of Consumer AI. Part 3: Time is Money

In Part 1, I showed that ChatGPT has pulled away in usage. 900M WAUs, ~70% market share, the only AI app on a trajectory toward core utility status. In Part 2, I showed that the engagement underneath those numbers is real. Improving WAU:MAU, a rare smile curve in retention, and stickiness metrics that rival Slack and Gmail at work and X and Spotify at home.

Those two posts were about Q in the Revenue = Price × Quantity equation. How many users, how often they come back, and whether the habit is real. This post is about P. What can you actually charge?

Time spent is the bridge between the two. In consumer technology, time is the raw material of monetization. Subscription businesses convert time into perceived value and willingness to pay. Advertising businesses convert time into ad inventory. Both start with the same input: how much of a user’s day does your product command?

Bottom line up front: I think the advertising revenue opportunity for leading consumer AI apps may be larger than the subscription opportunity. The reason is simple: consumer AI is accumulating the same raw material that powers the largest internet businesses, time and attention. The ad revenue equation is straightforward: Ad revenue = Total Time × Ad Volume × Price of Ads. Across these three variables, the data suggests:

Total time spent in AI apps is exploding. AI mindshare follows the same power law as the number of users, even adjusted for how much time each user spends.

Time per user is rising → large and growing ad volumes. AI apps trail consumer benchmarks but are starting to rival enterprise apps. ChatGPT is behaving more like a work and productivity tool than a social feed. That is a strong signal for the ability to increase ad loads over time.

ChatGPT queries have stronger intent signals than search → compelling ad pricing. More on this in Section 3 below.

Let’s dig in.

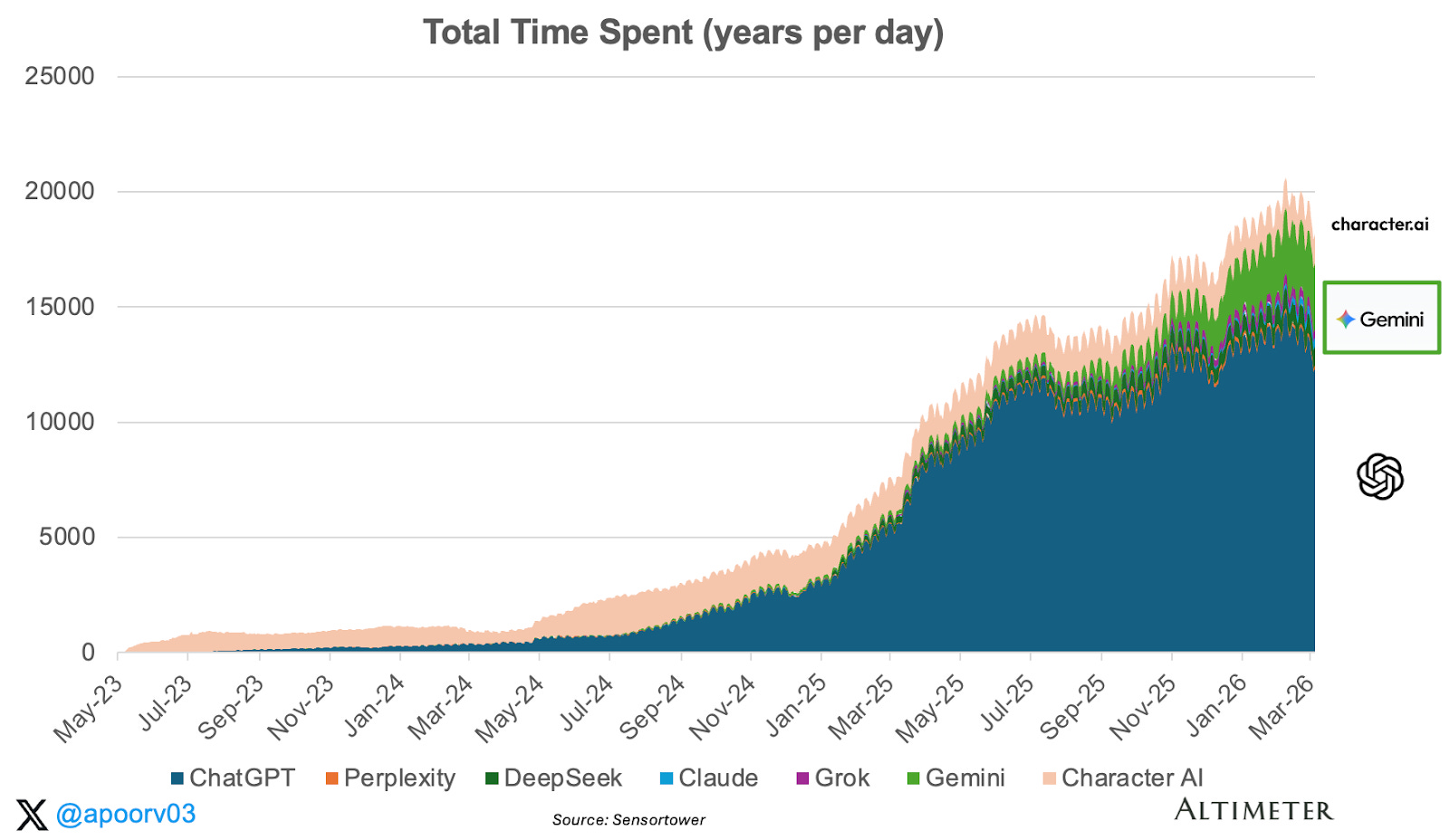

1. Total Time: ChatGPT owns 68% of Consumer AI’s attention

Total time spent in generative AI apps grew approximately 10x over the past two years and 3.6x in 2025 alone. No app category has scaled this fast.

A few things jump out. First, the inflection around January 2025 is striking. Total time spent roughly doubled in the first half of 2025, driven by ChatGPT’s expansion into voice, image generation, and search. Second, Gemini emerged around mid-2024 and has grown meaningfully, but remains a distant second.

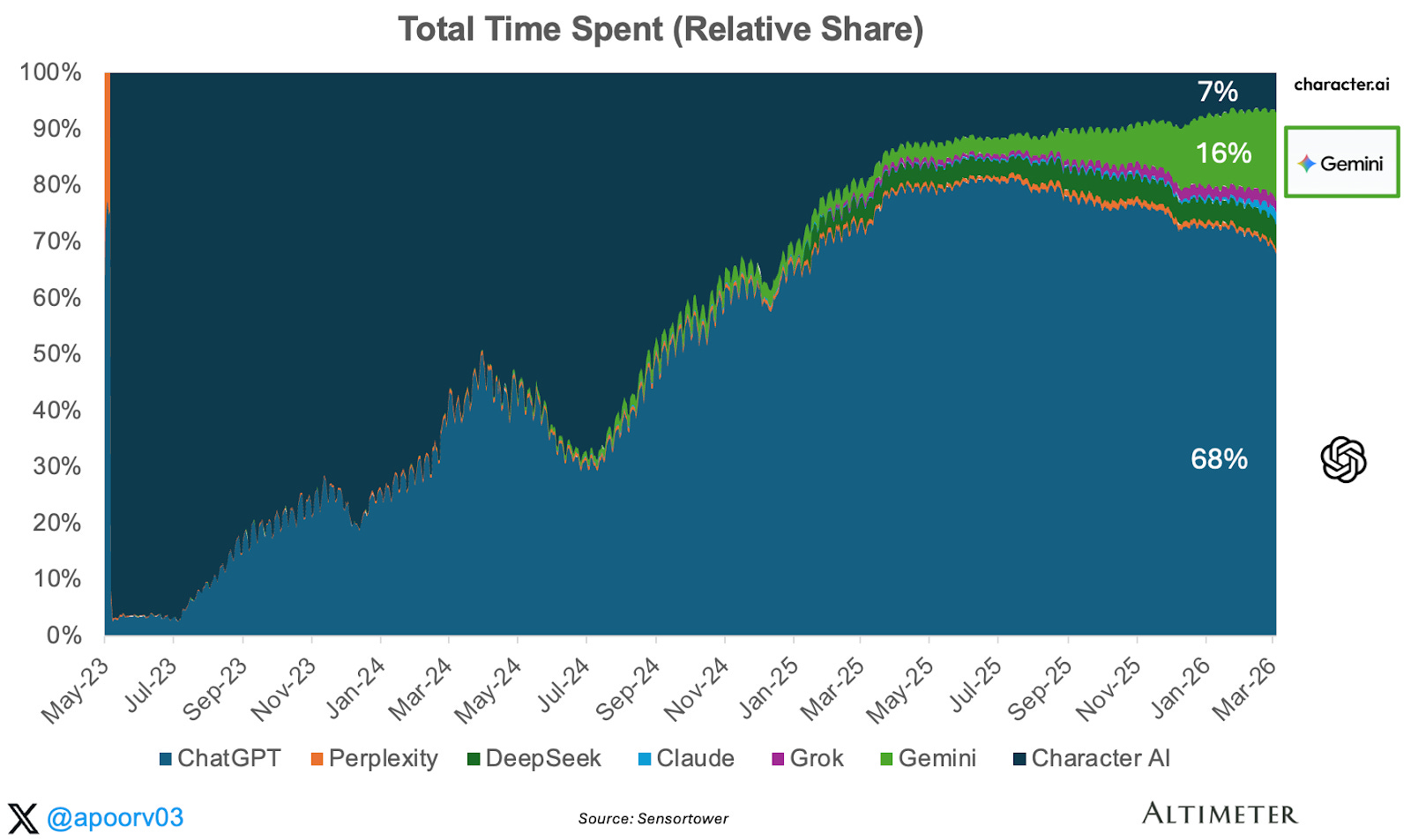

ChatGPT commands 68% of total AI time spent. Gemini is at 16%. Everyone else combines for roughly 16%. This concentration makes ChatGPT the most plausible place for the first scaled AI-native advertising franchise to emerge. It also helps explain why OpenAI is experimenting earlier and more aggressively with monetization than peers with smaller shares of attention. This is also important to note because you can’t really do advertising in a sub-scale platform.

Where users spend time is the real estate available to advertisers. And 68% of that inventory sits inside one product - ChatGPT. For advertisers evaluating AI-native ad spend, the concentration of attention in a single product is hard to ignore.

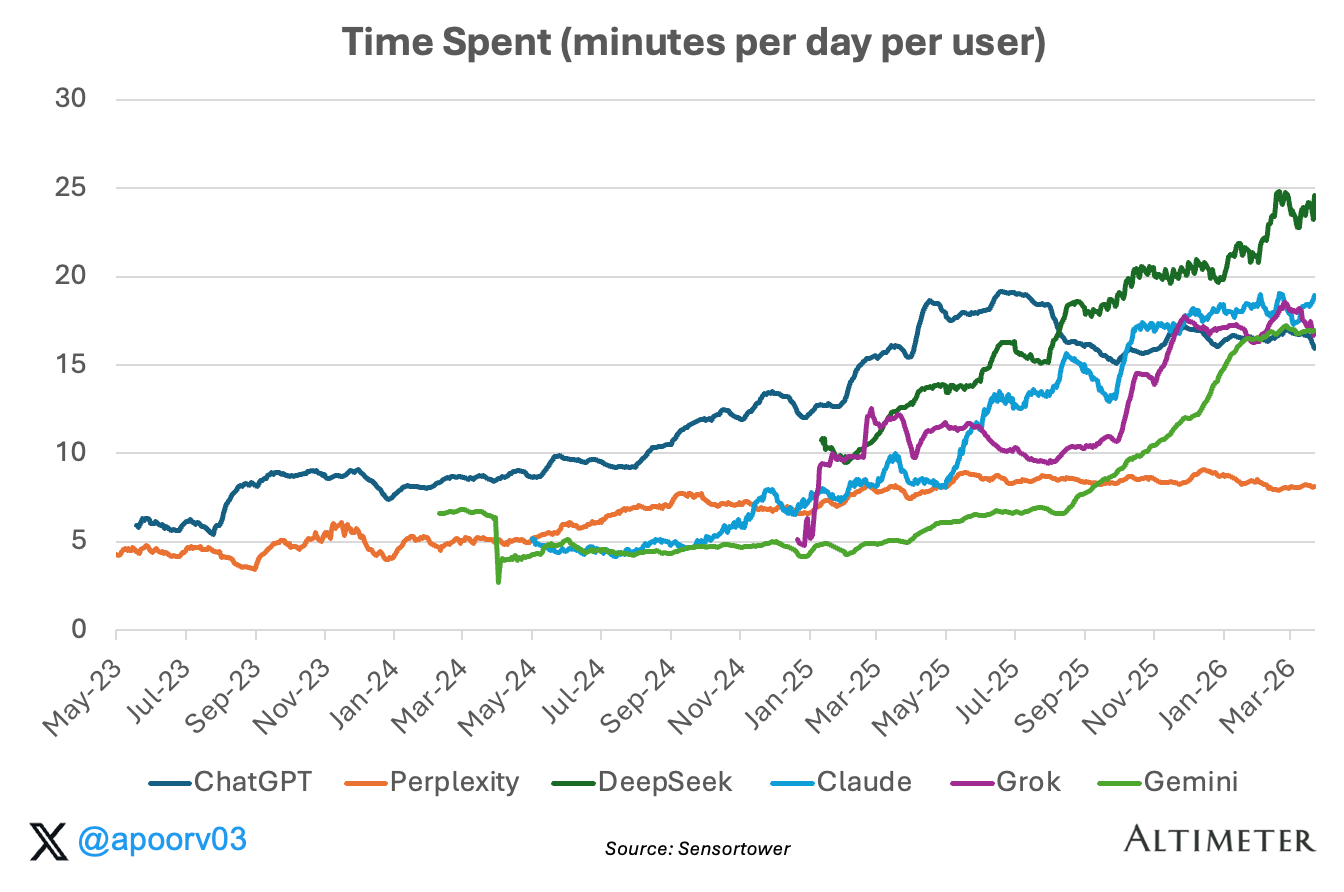

2. Time per user is rising. That means more surface area for ads.

Every AI app on this chart is trending up. ChatGPT has roughly tripled its time per user since early 2023. Claude, Gemini, and Grok have all climbed steeply over the past year. The trend is clear: people are spending more time in AI apps, not just downloading them and leaving.

But how much time, relative to what we already know about consumer and enterprise apps?

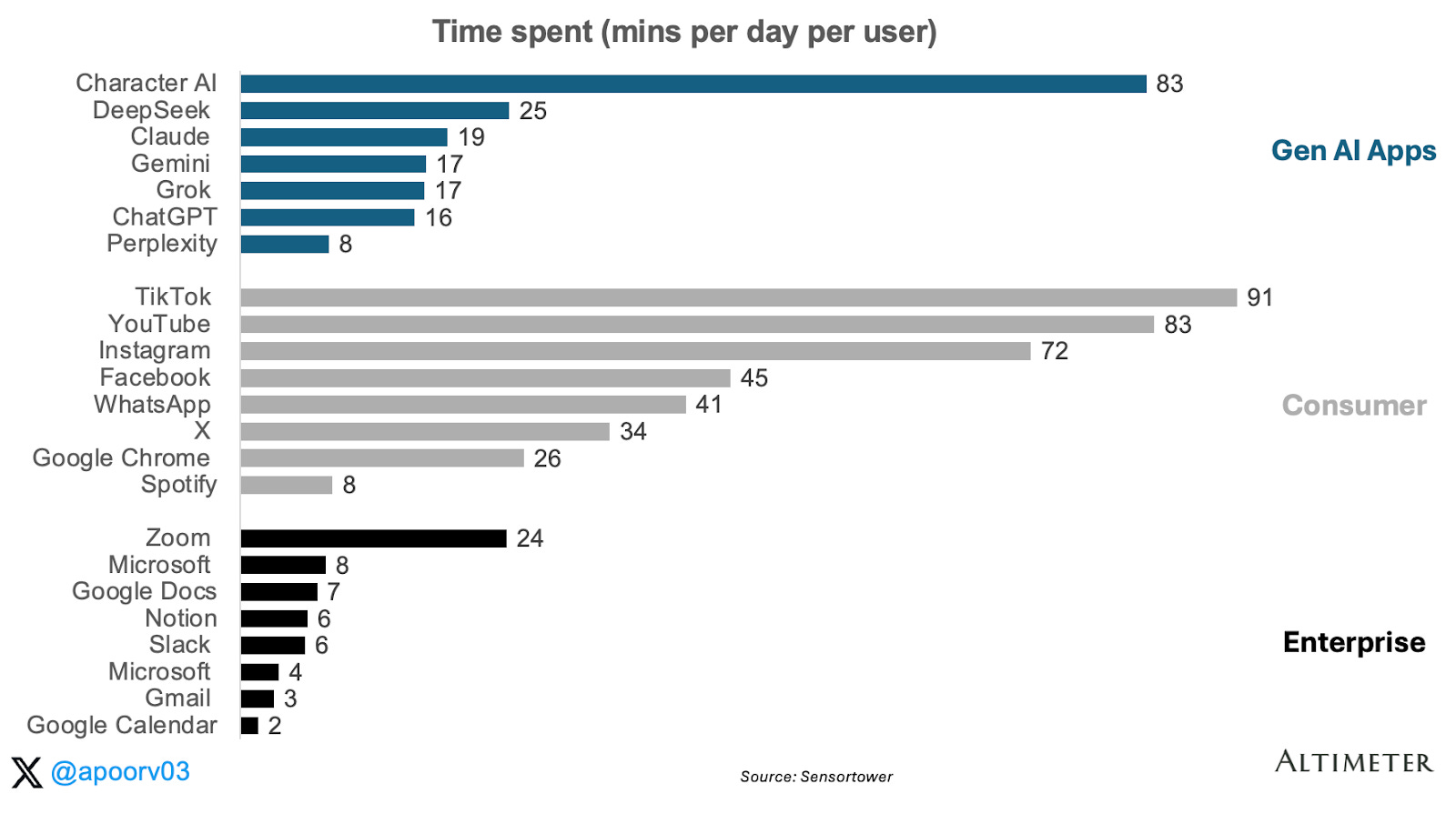

Versus consumer: still a lot lower. ChatGPT at 16 minutes per day is well below TikTok, YouTube, Instagram, and the rest. But this gap isn’t really a fair comparison because ChatGPT lacks the two things that drive massive time spent in consumer apps.

First, it has no social network effects. TikTok and Instagram are sticky in part because your friends, creators, and communities are there. The content is personalized to you and generated by people you follow. That creates a pull to keep coming back and keep scrolling. ChatGPT has none of that. There is no feed, no followers, no social graph.

Second, it has no dopamine loop. You don’t open ChatGPT to scroll through cat videos or see what your ex is up to. Consumer social apps are engineered for variable-reward engagement: you never know if the next swipe will be boring or hilarious, and that unpredictability keeps you glued. AI assistants are the opposite. You come with a specific task, you get an answer, you leave.

Versus enterprise: higher than most. The enterprise comparison is more useful, with one important caveat: this is mobile-only data from SensorTower, so desktop-heavy products like Slack, Gmail, and Google Docs are understated here. Even so, the signal is notable. On mobile alone, ChatGPT already looks like a high-frequency productivity utility. That matters because productivity products monetize well even at much lower time-spent levels than consumer entertainment apps.

Slack charges $7-12 per user per month. If AI assistants are already capturing this level of daily attention while operating at consumer scale, the monetization surface area is meaningful.

Rising time per user means two things for the revenue equation: more perceived value to support willingness to pay for subscriptions, and more surface area to serve ads. Both point in the right direction.

3. The revenue opportunity

3a. Why ads can outscale subscriptions

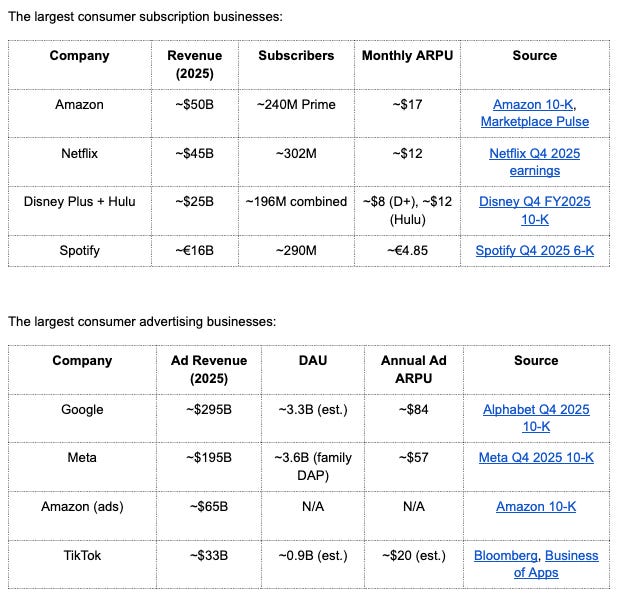

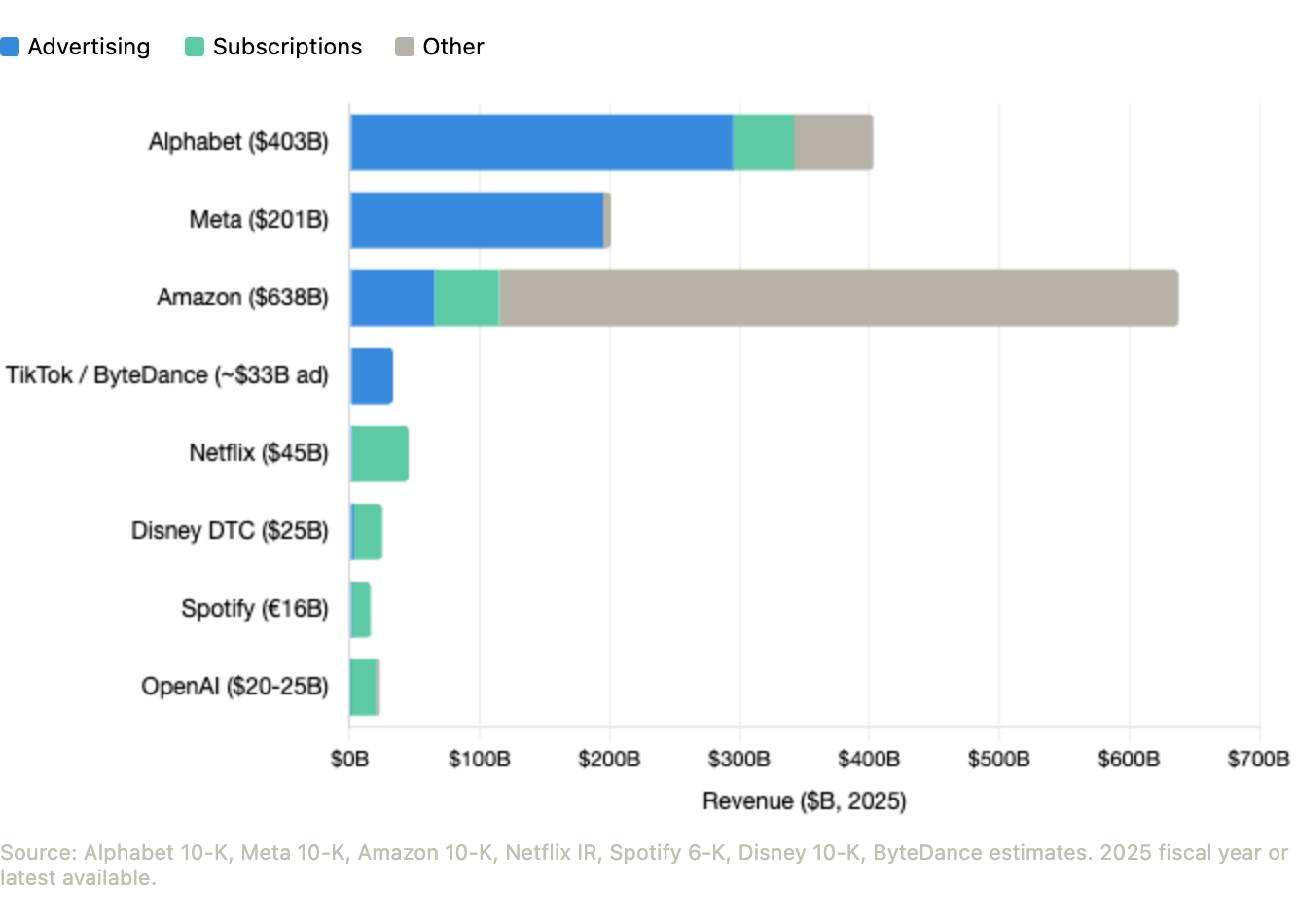

Now to the price side: what is all of this attention actually worth? At consumer scale, the two monetization models that matter most are subscriptions and advertising. The important point is not that subscriptions are weak. It is that the largest consumer internet businesses have historically monetized far more revenue through ads than through subscriptions.

The magnitude gap is the point. Google’s advertising business alone is roughly 5x Netflix’s revenue. Meta’s advertising business is roughly 4x. Even Amazon’s ad business, which barely existed a decade ago, is larger than Netflix today. The natural question is whether higher subscription ARPU makes up for the smaller paying base. For some businesses it does. But at scale, the larger monetized base from ads tends to win.

Alphabet and Amazon are particularly interesting because they have both models. In both cases, the ad business is larger than the subscription business, and growing faster. Netflix, Disney, and Spotify are almost entirely subscription. Meta and TikTok are almost entirely ads. OpenAI today is almost entirely subscription revenue, with some ad revenue from the recent launch across a fraction of their 95% free users in the US. That is an enormous pool of attention that is currently generating almost zero revenue. OpenAI is the first mover here, but the same free-user monetization question applies to every AI app with a large unpaid base.

3b. How AI attention gets priced

Ad revenue = Total Time × Ad Volume × Price of Ads

Total Time: We already know Total Time from Sections 1 and 2. ChatGPT has ~900M WAU, DAU:MAU of 45%, ~16 minutes per day on mobile.

Ad volume (or ad load): is a product decision. How many ads do you show per session? Google shows 3-4 ads per search results page. Meta shows an ad every 3-5 posts in the feed. ChatGPT currently shows at most one ad per conversation, and only for ~5% of mobile users. That restraint is smart for preserving trust, but it means the ad load variable is currently very low.

Price of ads (CPM) is the price advertisers will pay per thousand impressions. This is where it gets interesting, because not all attention is priced equally. CPM is ultimately a function of one question: will this user buy something? That breaks down into three things: intent (is the user actively making a decision?), attribution (can the advertiser trace the ad to a purchase?), and audience quality (does this user have spending power?).

The biggest ad franchises each lean on different strengths here. Google Search has a strong intent signal because when someone types “best mortgage rates 2026,” they are declaring a commercial intention in real time. CPMs of $15-200+ depending on category. Revenue per user of ~$84/year globally. Meta has weaker intent but massive time spent. Users scroll 30-90 minutes per day. Meta compensates with extraordinary targeting precision, inferring intent from behavior and people graphs. Revenue per user of ~$57/year. YouTube sits in between: mid CPMs, long sessions, video creative.

To summarize, Google sells intent. Meta sells attention. YouTube sells watch time.

3c. Where AI assistants fit - a ChatGPT case study

Let’s use ChatGPT as the test case since it has the largest free user base and the most ad data to work with. ChatGPT ad pricing will likely land closer to Google than Meta, and potentially advantaged in categories where conversational context improves commercial intent.

When someone opens ChatGPT and asks for a laptop recommendation, compares insurance plans, or plans a family trip, the interaction resembles search, but with richer context. The user often provides budget, preferences, constraints, and intent in a single prompt. That can make the commercial signal more legible to an advertiser, even if it does not automatically make every AI query more valuable than a search query.

I’d expect ChatGPT’s realized CPMs to be at least comparable to Google Search and potentially higher for certain categories. The early data supports this. OpenAI’s premium placements are priced at roughly $60 CPM, well above display advertising and in the range of high-intent search.

Today ChatGPT has ~800-900M free users (95% of WAU). If ChatGPT can generate $30 in annual ad revenue per free user, that implies $25B in ad revenue at current scale. For reference, Meta generates $57/user and Google generates $84/user, so $30 for a high-intent logged-in product is not aggressive.

The early data shows no impact on trust metrics, but the test is still early. Scaling ads 20x without degrading the experience that built the habit is the real execution challenge. The main reason this opportunity remains unproven is that not all AI time is commercial. A meaningful share of ChatGPT usage is informational, creative, or productivity-oriented rather than transactional. And unlike a feed or search results page, a conversational interface gives you fewer obvious places to inject ads without harming trust. So the upside is real, but the execution constraint is equally real: OpenAI has to monetize the habit without degrading the product that created it.

There is also a more optimistic possibility. AI does not just create ad inventory. It can create entirely new ad formats. Conversational ads, where the product recommendation is woven into the dialogue rather than bolted onto the side of it, could actually improve the user experience rather than degrade it. Imagine asking ChatGPT to plan a weekend trip and having it surface a relevant hotel deal within the conversation, informed by your unique preferences and memory. That is not an interruption. That is a feature. If AI enables hyper-personalization, agentic behavior, and truly conversational moments with brands, the advertising opportunity may not just be large. It may be meaningfully different from any ad experience that exists today.

3d. Why Google can wait

Google’s strategy is notably different from OpenAI’s. Google has repeatedly said it has no plans to run ads in Gemini. At Davos in January, DeepMind CEO Demis Hassabis said he was “surprised” that OpenAI was rushing forward with ads in ChatGPT. Google Ads VP Dan Taylor stated on X in December 2025: “There are no ads in the Gemini app and there are no current plans to change that.”

This is a strategic luxury only Google can afford. Google already has a $295B advertising cash machine in Search. It can subsidize Gemini as a loss leader, using the ad-free experience to grow users and deepen engagement while monetizing AI through its existing Search infrastructure (AI Overviews and AI Mode already carry ads). OpenAI does not have that luxury. With no separate cash cow to lean on, it must monetize the chat interface directly.

For now, Gemini monetizes only through subscriptions. That is a much smaller revenue opportunity per user than what OpenAI is building with ads + subscriptions. But Google is playing a different game. It is protecting the assistant to retain users while aggressively monetizing the search results page. Whether that strategy holds as free-user inference costs rise and Gemini’s user base scales past 750M MAU is an open question. At some point, the economics of running a massive free AI assistant may force even Google’s hand.

Putting it all together

This series asked a simple question: is consumer AI just a lot of usage, or is it becoming a real business? Part 1 showed the reach. Part 2 showed the habit. Part 3 suggests the monetization opportunity may be larger than many people appreciate.

The underappreciated point is that leading AI assistants, ChatGPT foremost among them, already have properties that the largest consumer internet businesses monetize best: scaled, recurring attention. Roughly 95% of its weekly active users are still free, which means most of that attention is barely monetized today.

That does not guarantee an ad business on the scale of Google or Meta. Conversational interfaces are harder to monetize cleanly, and trust is the product’s most valuable asset. But if OpenAI can prove that ads can live inside a high-intent assistant without breaking the user experience, the long-term advertising opportunity could end up larger than the subscription business. And if that happens, the real strategic question for Google will no longer be whether Gemini should stay ad-free. It will be how long it can afford to.

Thanks to Sarah Friar and Fidji Simo for reviewing drafts of this article and series.

Sources used in this post include Sensortower.

The information presented in this newsletter is the opinion of the author and does not necessarily reflect the view of any other person or entity, including Altimeter Capital Management, LP (”Altimeter”). The information provided is believed to be from reliable sources but no liability is accepted for any inaccuracies. This is for information purposes and should not be construed as an investment recommendation. Past performance is no guarantee of future performance. Altimeter is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. Altimeter and its clients trade in public securities and have made and/or may make investments in or investment decisions relating to the companies referenced herein. The views expressed herein are those of the author and not of Altimeter or its clients, which reserve the right to make investment decisions or engage in trading activity that would be (or could be construed as) consistent and/or inconsistent with the views expressed herein. This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.

First of all — great post and fantastic MS&E 435 course on YouTube.

One angle I keep scratching my head on related to the revenue conversation: what if leading AI platforms launched their own agent marketplaces — the same way Apple and Google built the App Store and Google Play?

Most users have not built their own agents. Not because the technology is inaccessible, but because doing it well requires knowing how to structure agent logic, minimise token consumption, and handle the security implications of autonomous agents acting on your behalf. That is a real literacy gap — and a real business opportunity.

A platform-native agent store solves this cleanly: vetted, efficient, pre-audited agents with defined permissions. The security angle alone makes it compelling for enterprises of all sizes. Leading AI companies could publish their own agents (less ROI here) or open the platform to third-party developers — with the marketplace vetting all uploads to screen for malware and other security risks.

Really enjoyed these posts for week 1 of your ms&e 435 course. I particularly liked your value accrual model in posts 1 and 2 that suggest the big long term opportunity is still at the app layer. The time series data from past industry booms starting at the Semis and moving up the stack to the app layer was very interesting to see, and suggests a similar pattern may emerge over the next decade in the AI industry.

It would be very interesting to see the updated usage data to account for the first ~half of 2026, I'm curious to see how Anthropic's recent growth is reflected in mobile app usage relative to OpenAI's supposed stagnation.

It would also be very interesting to take a look at the relative opportunities of generative AI in the consumer context vs. business context. There seems to be a power law where the top business spenders are relatively price insensitive and willing to spend aggressively on token consumption. Anthropic clearly seems to have taken notice of this!